Building state capacity isn’t an ism.

America’s Advantage Over China is—or Was—Innovation

Time is pressing to turn our tech Titanic around.

Sen. Rubio’s remarks on industrial policy call for a shift in focus from China’s unfair trade practices to the need to restore America’s vulnerable manufacturing base. As he told the National Defense University:

While it may be true that China is “breaking the rules” or that Chinese companies are engaging in “unfair competition” against the American order, the fundamental challenge will not simply be solved by some future trade agreement…The industries that China intends to dominate are the very ones that will create the dignified and productive work Americans need for us to remain a strong nation.

He added:

The depletion of America’s manufacturing sector has left us with a tremendous national security vulnerability. I am not advocating for a government takeover of our means of production. What I am calling for us to do is remember that from World War II to the Space Race and beyond, a capitalist America has always relied on public-private collaboration to further our national security. And from the internet to GPS, many of the innovations that have made America a technological superpower originated from national defense-oriented, public-private partnerships.

To paraphrase Leon Trotsky: you may not be interested in industrial policy, but industrial policy is interested in you.

Sen. Rubio’s intervention is a welcome addition to a growing body of opinion that trade war is not enough: the United States requires a concerted national effort to assert technological leadership and rebuild its manufacturing base. Other contributions to the debate have come recently from former House Speaker Newt Gingrich, former NSA Director Admiral Michael Rogers, Hudson Institute researcher Arthur Herman, and others, including this writer.

Trade Versus Industry

Sen. Rubio offers two motivations for industrial policy: first, the need to maintain America’s strategic superiority in face of a challenge from China, and second, the damage to the lives of American workers and their communities due to the loss of industrial jobs. It is vital to distinguish between these policy issues. Subsidizing domestic steel production won’t prevent China from leapfrogging the U.S. in telecommunications technology, and high-tech R&D to defend against Chinese hypervelocity missiles won’t reverse employment losses in the rust belt.

The Chinese model is not in principle new. America subsidizes sports stadiums; Asia subsidizes chip fabrication plants. The so-called “Asian model” of industrial development began with the 1868 Meiji Restoration in Japan. Next came the postwar Singapore and Korean models, then Deng Xiaoping’s 1979 market reforms in China, which themselves emulated Singapore’s industrial policy. The Asian model treats capital-intensive industry as infrastructure and applies subsidies in the same way that the United States subsidizes airports, water treatment plants, and sports facilities.

During the 1980s, the United States used tariffs, quotas and currency policy to stem the loss of American manufacturing jobs to Japan. Japan is an American ally and its economy and population are much smaller than that of the United States, whereas China has 1.4 billion people. Its economy is roughly the same size as America’s and growing three times as fast.

As former National Security Agency head Admiral Michael Rogers observed earlier this month, China “represents a significant diplomatic, political and military challenge. But what makes it so different is it combines all of that with this significant economic capability. We have also not had a near-peer economically who is also such a competitor or potential adversary.”

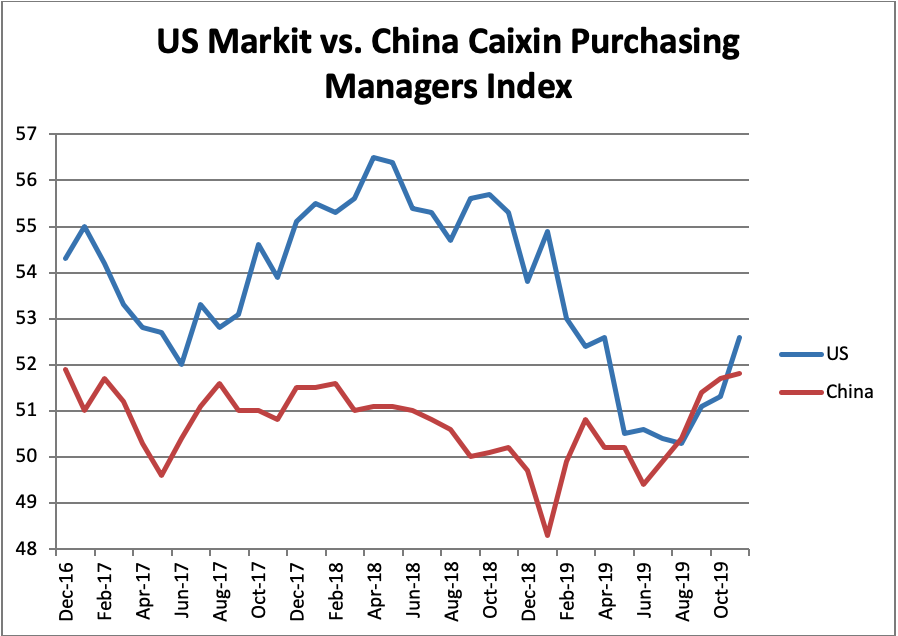

The shift in attention toward industrial rather than trade policy is overdue. The Trump Administration’s tariffs on Chinese imports resulted in a global manufacturing recession, including in the United States. The Markit Purchasing Managers’ Index for U.S. industrial production stood at 56 in July 2018 when the U.S. imposed its first round of tariffs on Chinese imports. By August 2019 it had fallen to 50, indicating zero growth, while the Federal Reserve Board’s Index of Industrial Production registered declines during the first three quarters of 2019. A similar gauge for Chinese industrial production also indicated contraction during the first half of 2019 before recovering during the third quarter. Similar declines occurred in Western Europe, Japan, South Korea, and Taiwan.

Because industrial supply chains are distributed globally, the trade war prompted businesses to postpone investment decisions until the dust settled. Declining business fixed investment reduced U.S. GDP growth during the second and third quarters of 2019.

The data show clearly that the trade war hurt the United States as well as China, which nonetheless continues to grow at around 6% per annum versus about 2% in the United States. The Trump Administration wisely negotiated a truce in mid-December 2019.

Efficiency Versus National Interest

Meanwhile the Administration’s efforts to prevent China’s Huawei Technologies from dominating the global rollout of Fifth Generation (5G) mobile broadband have gained little purchase.

In April 2018, the U.S. banned exports of American components to the Chinese telecom equipment firm ZTE after ZTE was found in violation of Iran sanctions. That effectively shut the company down until the U.S. allowed sales under stringent conditions. Before the end of 2018, Huawei introduced its Kirin chipset for high-end mobile handsets. A year later, Huawei appears able to produce handsets, mobile base stations and other equipment without U.S. components. Huawei has shifted its sourcing to Taiwan and Japan.

Huawei claims that it will ship 2 million 5G base stations by 2020, and claims to have signed contracts with 50 telecom providers to sell 5G equipment. Except for Japan, the whole of the Eurasian continent is doing business with Huawei, despite urgent remonstrations from the U.S. government and threats to suspend the sharing of intelligence. Japan and Taiwan meanwhile are selling components to China that the United States has banned, and thousands of Taiwanese engineers are staffing China’s aggressive plans to dominate world chip production.

Rather than constrain China’s dominance of telecommunications equipment, American export controls elicited a successful drive for Chinese self-sufficiency. America’s relative position, in short, has deteriorated drastically during the past year. Without an American national champion to contend with Huawei, America’s efforts to suppress Huawei’s dominant position have failed.

No one is more surprised at this outcome than the Chinese themselves. A senior officer of Huawei asked me: “Why didn’t the United States just have Cisco buy Ericsson, and create a national champion to compete with us?” (Cisco used to dominate the market for internet routers.) The answer is that Cisco’s return on equity last year was 36% while Ericsson’s was -4%, as the Swedish telecommunications producer struggled to keep up with its Chinese competition. A merger would bring down Cisco’s equity price, and American managers focus on little but returns to shareholders.

Sen. Rubio contends that “responding to this challenge will require us to reject the fundamentalism that argues that the greatest virtue in American policy is to maximize ‘efficiency.’ The market will always reach the most efficient economic outcome, but sometimes the most efficient outcome is at odds with the common good and the national interest.” That statement is entirely correct, but it raises two major problems:

- If the U.S. government makes demands on corporations that reduce efficiency, e.g., by forcing a merger between Cisco and Ericsson, why should the costs be borne disproportionately by a specific group of Americans, in this case Cisco’s shareholders?

- If the United States reduces the efficiency of its economy in the interests of national security, job preservation, or other national goals, how will that affect the creditworthiness of the United States? We currently run a federal deficit of $1 trillion and borrow about $500 billion a year from the rest of the world. We owe $17 trillion to the public and have an additional $46 trillion in unfunded obligations from entitlement programs. Nonetheless the Federal government is able to borrow at or close to the lowest rates in history, because investors have long-term confidence in the efficiency of the U.S. economy. There is a limit past which a reduction in efficiency will undermine confidence.

How America Lost Its Digital Dominance

In the past, massive public support for basic R&D led to the creation of entirely new industries.

The 1980s were a golden age of employment and wage growth, yet employment at Fortune 500 companies declined, and new businesses in nascent industries more than compensated. Data processing was the industry that showed the biggest absolute gain in employment. The greatest employment and wage income gains came from industries made possible by federal R&D support, but whose emergence could not have been predicted in advance.

In 1983, an official of Reagan’s National Security Council, Dr. Norman Bailey, asked me to prepare an estimate of the civilian economic gains that might accrue from defense R&D. I offered a positive assessment, but wildly underestimated the actual outcome: the entirety of the digital age came about as a result of DARPA investments. For example: The fast, light and cheap CMOS chips that powered the digital revolution were supported by a grant to RCA Labs from the Defense Advanced Research Projects Agency (DARPA). DARPA wanted fighter pilots to have the computational power to perform weather analysis in the cockpit; only afterward did the Defense Department realize that CMOS chips made lookdown radar possible.

The semiconductor laser also was invented through a DARPA grant to RCA Labs, whose original purpose was nocturnal illumination of battlefields. Only later did the industry realize that the technology made possible laser-powered optical networks. From this arose the cable television industry among many others.

Digital technology is now the key to military strength, but America’s capacity to manufacture the major components of digital systems is disappearing. America shipped 25% of the world’s semiconductors in 2011 but only 10% in 2018. Henry Kressel and I wrote last year in the Wall Street Journal that

The U.S. pioneered the technology that made today’s advanced weapon systems possible. But America’s competitive advantage in the digital economy is eroding at an alarming pace, along with its domestic high-tech manufacturing capacity. The majority of electronic systems first invented in the U.S. now are designed and made overseas, mainly in Asia. With few and dwindling exceptions, the U.S. no longer makes things like flat-panel displays, memory devices, light-emitting devices, lasers, imaging chips for digital cameras, and computer system packaging software.

As the manufacture of these component technologies has migrated offshore, so have many key systems suppliers. Intel is the only remaining U.S. company capable of fabricating high-density, high-performance computer chips in America. International Business Strategies estimates that investors are pouring $50 billion a year into advanced chip production facilities in Asia, more than 10 times the level of domestic spending.

Huawei certainly stole technology in the past, including computer code from Cisco. In 2004, Huawei settled a suit by Cisco, then America’s dominant provider of telecommunications equipment, for alleged technology theft. Today, Huawei spends more on R&D than its competitors combined and owns 30% of the patents relating to 5G Internet. Our most urgent concern is now no longer the theft of American intellectual property but the creation of Chinese intellectual property.

Not just 5G mobile broadband, but also the technologies that it makes possible, threaten to give China a decisive lead in disruptive technologies throughout the 21st century. At Huawei’s Shanghai Connect conference in September 2019, industry leaders elaborated some of the possibilities: for example, factory-floor robots that could communicate instantly with each other and, with the aid of machine learning, formulate production plans faster and more efficiently than human engineers. The chief technology officer of the leading European robotics firm ABB described a near future for mining in which no human being will go underground, because technicians above the surface will manipulate remote-control mining machines while wearing augmented reality helmets.

Most important, Huawei’s advantage in rolling out 5G mobile broadband may give the Chinese firm a decisive edge in collecting key data—on human health, consumer transactions, shipping and warehousing, traffic patterns, and so forth. Data is the key to dominance in artificial intelligence.

For example, Huawei expects to link 500,000,000 people to its cloud-based medical records system during the next 10 years, including genetic data, treatment histories, and real-time uploads of vital signs, EKG readings, and so forth through smartphones. Huawei is seeking to become the dominant mover and repository of data that would allow China to dominate Artificial Intelligence.

Industrial automation, big-data analysis of health information, and so forth are American rather than Chinese concepts. What gives Huawei a decisive advantage over prospective American competitors is its dominance in building the mobile communications networks.

Sen. Rubio decries China’s “use of state-associated firms like Huawei to entice foreign nations into exploitative contracts that give China access to foreign nations’ critical national security data.” That is the view of the U.S. intelligence services, who like all intelligence services exaggerate the importance of secrets because it is their stock-in-trade. Far more threatening to American interests is the likelihood that the whole world will give its data to Huawei freely, in return for the benefits of A.I.

Huawei spends close to $20 billion a year in R&D, more than its competitors combined. Considering the strategic benefits that China derives from Huawei’s dominance in broadband technology, that is a trivial sum.

After the 2000 tech stock crash and recession, American investment shifted out of manufacturing and hardware, and into software. The advantage of software is infinite scalability: the marginal cost of adding a customer is zero, and the great software firms that achieved strong network effects—Google, Facebook, Microsoft, and others—generated a level of profitability unprecedented in market history. Asians were willing to subsidize manufacturing industry to provide cheap hardware for the American market. American software companies were happy to concentrate on high-margin software and leave lower-margin manufacturing to Asia.

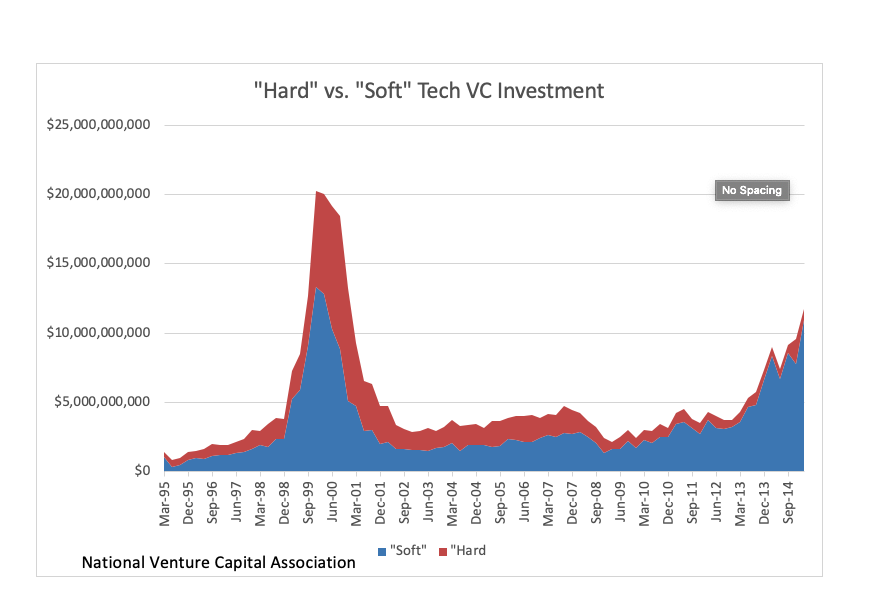

Even at the level of seed capital, virtually nothing is left in the high-tech manufacturing pipeline. An insignificant fraction of U.S. venture capital commitments is directed to information technology hardware.

This is an enormous turnaround from the late 1990s, when the telecommunications boom motivated a wave of venture investment in I.T. hardware. By 2015, hardware investment had all but disappeared.

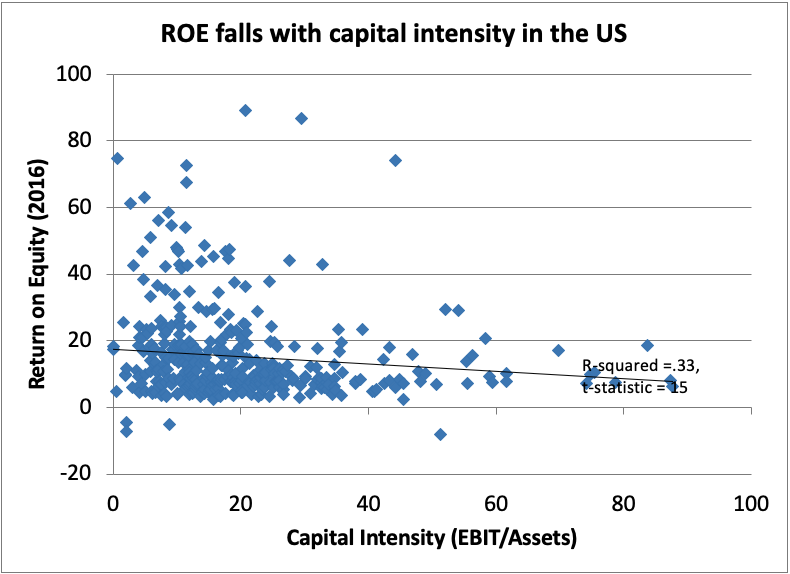

We observe a negative relationship between capital intensity and return on equity among the companies in the S&P 500 index. “Capital light” has worked out well for American business, because America is able to source cheap hardware in Asia. Data in the chart below are from 2017.

Among the constituents of the MSCI China equity index, we observe the opposite: There is a strong positive relationship between return on equity and capital intensity (data from 2017).

Almost certainly, the high profitability of capital-intensive Chinese companies reflects state subsidies for capital investment.

Rebuild R&D

What sort of industrial policy should the United States adopt? The broader problem of rebuilding American manufacturing requires changing corporate behavior.

Cutting off imports from China or other Asian exporters isn’t a good option. The American supply chain is so dependent on Asian manufacturing that disruption would be devastating. The Trump Administration was wise to rescind the 25% tariffs on $350 billion of Chinese goods originally scheduled for December 15.

We cannot protect employment simply because it used to be there. Employment in some industries will shrivel because of changing technology, regardless of trade agreements. I support subsidies for jobs in some cases, but the costs of subsidies in capital-intensive industries such as mining and metallurgy is prohibitive.

But we cannot afford not to subsidize key technologies, especially where they bear on national defense.

I have advocated a crash program on the part of the United States and its NATO partners to retake the high ground in telecommunications technology. We have seen that it is not enough to admonish our allies against working with Huawei. We should do whatever it takes to create an alternative, as an emergency measure.

Turning this supertanker around will take ten years and roughly $1 trillion of additional spending. Tax incentives and subsidies will be required, above all for R&D. Much more than money is required. Federal R&D peaked in 1987 as a percentage of GDP at 1.23%, or the equivalent of $250 billion in current dollars. In 2017, the United States spent only half that amount, or $127 billion, in federal R&D. We couldn’t spend $250 billion today if we tried to.

The corporate laboratories that received the lion’s share of DARPA grants—at Bell, General Electric, RCA, IBM, Hughes and many other firms—have ceased to exist. The national laboratories have shrunk. If the major corporations wanted to revive their laboratories, they couldn’t find the engineers; if the universities wanted to train more engineers, they couldn’t find the faculty (see Edward R. Dougherty, “The Decline of American Science and Engineering,” American Affairs, Spring 2019).

We will require educational reforms along the lines of the Eisenhower National Defense Education Act to address the shortfall of skills. Meanwhile China graduates four times as many STEM bachelor’s degrees and twice as many STEM doctorates as the United States, and the gap is widening.

There are some things that we can and should do immediately. A good place to start is strict enforcement of domestic content for defense technology. We cannot afford to source chips, displays, and other sensitive defense electronics from overseas. An emergency program should be put in place to produce semiconductors, sensors, displays and other high-tech defense goods. That will require direct subsidies, but these are justifiable on national security as well as economic grounds.

We cannot return to where we were in 1980. We should aim for where we want to be in 2030. As I wrote two years ago in American Affairs:

Federal R&D is effective not merely because it is federal…. On the contrary, governments frequently waste R&D funds on white elephant projects such as Solyndra, the California-based solar power venture that defaulted on a $535 million U.S. government loan. The F-35 and other poorly conceived acquisition programs also absorb large amounts of R&D funding. In contrast to these incremental projects, R&D that is focused on game-changing breakthroughs is the most productive. And the technological innovation it makes possible becomes truly transformative only when entrepreneurs effectively commercialize it. Kennedy’s moon shot and Reagan’s Strategic Defense Initiative had such lasting economic reverberations because they were accompanied by tax cuts and regulatory relief that made it easier for entrepreneurs to capitalize on basic scientific innovations. The Trump administration has already proposed aggressive fiscal and regulatory measures to improve incentives for investment. Neither innovation nor investment alone is enough, however; the innovations must turn into investment and employment in the United States.

There is a clear division of labor between the public sector and the private sector. Few if any of the game-changing inventions of the 1950s through the 1980s would have emerged—or emerged as early as they did—without federal R&D funding. Once the technology is invented, though, private investors must bear the brunt of the risk. Conventional industrial policy is the worst approach. It allows bureaucrats to create vested interests in existing industries, and it creates incentives to suppress new technologies that might threaten investments undertaken by political cronies.

There is a strong case, however, for using government funds to seed new companies that can develop innovative technologies. In an ideal world, the venture capital community would assume this function. But in the real world, the requirements of defense R&D and production require public funding.

The unintended consequences of federally sponsored R&D vastly exceeded the expectations of the projects’ initiators. The economic spinoffs of the technologies invented for urgent national security reasons had incalculable impacts on growth and productivity. None of this could have been pre-programmed. Innovation is unpredictable by definition. The greatest lesson we can draw from both the Kennedy space program and the Reagan Strategic Defense Initiative is that the most productive investments are the ones that test the frontiers of physics.

We will never match China in absolute numbers of scientists and engineers. China’s economy will be larger than ours in absolute terms. We have one decisive advantage, though, and that is America’s genius for innovation. Industrial policy should focus on fostering innovation, as it did under the aegis of the Apollo Program and the Strategic Defense Initiative.

The American Mind presents a range of perspectives. Views are writers’ own and do not necessarily represent those of The Claremont Institute.

The American Mind is a publication of the Claremont Institute, a non-profit 501(c)(3) organization, dedicated to restoring the principles of the American Founding to their rightful, preeminent authority in our national life. Interested in supporting our work? Gifts to the Claremont Institute are tax-deductible.

Also in this feature

Don’t remake America: reinvent it.

America thrives best free from market worship.

Actual policymakers have to do that.

The fix demands more than blame for Beijing.

Congress Should Join the Discussion Senator Rubio Has Begun.